Published On Jan 6, 2015

MIT 18.S096 Topics in Mathematics with Applications in Finance, Fall 2013

View the complete course: http://ocw.mit.edu/18-S096F13

Instructor: Kenneth Abbott

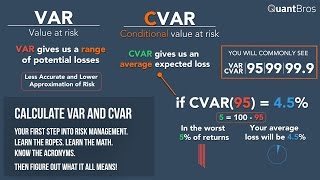

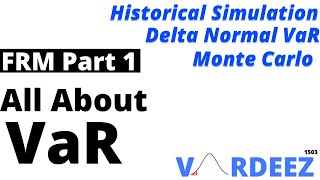

This is an applications lecture on Value At Risk (VAR) models, and how financial institutions manage market risk.

License: Creative Commons BY-NC-SA

More information at http://ocw.mit.edu/terms

More courses at http://ocw.mit.edu

show more